*This post may contain affiliate links. As an Amazon Associate we earn from qualifying purchases.

Why even both asking yourself any spending questions at all? Well, you know the saying “buyer’s remorse?” It’s that feeling we get when we spend a lot of money on something and then regret it. We might feel like we wasted our money, or just wish we had done more research before buying. Unfortunately, this happens to all of us at one point or another. To avoid buyer’s remorse, you need to be asking yourself some questions before you buy anything!

Let’s not deny the obvious. Buying things invokes a feeling of happiness, even if it’s only temporary. Did you buy a new purse for the upcoming summer months? Fly high on that purchase, my dear because that purchase may soon lose its sparkle and that feeling of wanting to buy the next big trend will be knocking at the door. Don’t worry. Each one of us is guilty of that. The good news? There are ways to help one figure out whether a purchase is a need, a want or if there is truly enough cash flow in your account to even be really thinking about purchasing at all.

Why is it important to think before you spend money?

It’s important to think before you spend money because it will help with budgeting. You can begin by thinking about your savings goals and how much of each paycheck should be allocated towards them. It also helps to have a list of other things that need to get done for the month, like car insurance or property taxes, so as not to overspend on unnecessary items. Thinking before spending money is vital for one’s finances to succeed long term.

The more pressing question is whether something needs immediate attention; if there’s an emergency at hand such as being out of work for several months consecutively or having medical expenses from surgery then these types of emergencies take precedence when it comes down to making that spending choice.

Related Article: 10 Best Tips for Creating a Budget That Works

10 Questions to Ask Yourself Before Spending Money

The urge to spend always seems to heighten at different times of the year for everyone. Why is that? Is it the excitement of a fresh start? Is it a barrage of ads aimed at invoking desire from us? Is it the looming tax return that you are anticipating…already planning on how to spend it before you get it? Whatever the source of our need to buy (or want), it’s important to pause before spending, be sure it’s what YOU are wanting to do, not another reason.

Let’s not deny the obvious. Buying things invoke a feeling of happiness, even if only temporary. Did you buy a new purse for the upcoming summer months? Fly high on that purchase, my dear..that purchase may soon lose its sparkle and that feeling of wanting to buy the next big trend will be knocking at the door. Don’t worry. Each and every one of us is guilty of that. The good news? There are ways to help one figure out whether a purchase is a need, a want or if there is truly enough cash flow in your account to even be really thinking about making a purchase at all.

- STOP ! Anytime the urge to spend money hits, try asking yourself these 10 questions to better understand the need to spend money:

What emotion am I feeling right now?

Maybe, just maybe, you are an emotional spender. Loving life? Let those dollars fly! Feeling blue? Buying a new pair of shoes sounds like an awesome pick-me-up in your mind. Boil it down and ask yourself how you are feeling at that moment. You may be surprised at how your mood influences your spending.

How great is that pair of new shoes are going to make you today? Play fortune teller for a moment and see if 6 months from now will they still make you smile when the stitching starts to wear or the shine fade? Are they now the shoes at the back of the closet or buried under the bed?

Some people are emotional spenders, some are emotional eaters, we all have weaknesses. It’s learning to know yourself better and weigh out if this is truly going to make you happy or just be a quick fix.

Possibly a less impulsive purchase would be exactly what is going to make you happy longer, give that some weight in your choice.

Knowing your emotional spending habits can mean making much better spending choices.

Do I really need this item?

It’s a hard question to ask, but necessary. Do you really need another pair of boots? Maybe, maybe not. Only you can ask, and answer, that question honestly.

A “Need” is a necessity. Necessities in budgeting are items like rent or mortgage, utilities, food, transportation.

A ‘Want” is more like a ‘splurge’ item. Something you save for and try to anticipate the purchase as much as possible.

For example: Tires on your car are a ‘need’ but the pinstriping is a ‘want’.

How many hours did I have to work to pay for this purchase?

I LOVE asking this question. It really helps put things in perspective. If you have your eye on a TV, look at the purchase price and divide your hourly wage into that. You will then have factual information to know that you worked X amount of hours to be able to buy that TV. Was it worth it?

Try thinking about it this way: If you were offered a brand new TV valued at $1,000 and someone said you can work for the TV for 75 hours of actual ‘work’ would you do that extra on top of your regular job? Well, for me the answer is oh heck NO! I’ll wait another year or two or have a yard sale to earn the extra cash.

Placing a value on yourself, your hard earned money is always worth while to stop and take a moment to give consideration to. YOU worked hard, spending carelessly isn’t showing much respect to yourself and your hard earned wages.

Could I save money buying this elsewhere?

Refuse to settle for the first price you see. Shop around, pull out your phone, tablet, or laptop, and price compare.

Take into consideration rebate/ cashback programs, store loyalty rewards. Personally, I get back cash regularly by only shopping with cashback programs. In addition, I’m still earning rewards from the store and using those towards future savings. Combine your resources for the ultimate savings.

Always check reviews too! Saving a ton on a product that is known to have a mile-long list of complaints is just throwing your money away. Don’t be that person.

Do the research and find out when this is a ‘seasonal’ product. Try searching ‘Best time to buy” in google and see if holding off a week or month could save you hundreds! Save that money!

Is the money to cover this in my account?

Seems common sense, but some people don’t honestly know the balance in their account. If you don’t have the money, you can not buy it.

The question is so simple—is there enough cash on hand for me to purchase something I want or need at this moment? It doesn’t matter how much of your paycheck goes into savings every week if all of it isn’t readily accessible you’ll need to wait until you can have the money where you can access it for the purchase.

Better yet, check your budget on a regular basis, weekly is perfect! You’ll be sure to know what you have , where it is and what is available.

What is the lifespan of the item I want to buy?

What is the lifespan of the item I want to buy? Do you really need a $75 bottle of wine or can it be replaced with something cheaper that will last longer based on how long you plan to use it for and what your budget allows? These are things that should be considered before buying!

In contrast, making that $75 car repair could mean many months or even years of being able to get to work safely on time. Thus securing your income.

Where else could I use this money?

Do you have monthly required bills such as utilities, rent, mortgage, insurance? Check any recent new bills too you may have forgotten to update your budget with. Go back to your previous 8 weeks on your bank statement, you may just find something you forgot you committed monthly to. (this is also a great time to update your budget!)

Is your emergency fund fully funded? Have you paid off your debt?

Can I borrow (or rent) this item instead of buying it?

A great question to ask when looking at one-use potential items such as tools or other equipment. Do you really only need to use the staple gun for one project that will take about 10 minutes and then so no future needs or use for it past that? Message some friends and family and see if anyone has one that you can borrow for the day instead of purchasing something that will be one and done.

This is one of those things my husband lives by. He has a mental list of who has what tools he can borrow and in turn he has tools he’s purchased (when needed more often) that he can lend to others.

My cousin is remodeling and she has no long-term needs for a tile cutter or miter saw, so she reached out and the family will be able to lend her these tools.

Heck we teach our kids to share, we can set a great example here!

I’ve always wanted to go glamping but honestly don’t think it’s something I’d want to do often, maybe once a year. It makes no sense for us to look into purchasing a large 5th wheel or other camper. We would be much better suited to rent for the 3 days a year we would want.

Borrowing first whenever possible and renting as an option should be part of your ‘go to’ arsenal of resources.

What will my significant other say?

Do you share a joint account with someone else? Make certain that the lines of communication are open in regards to purchases since the money in the account is linked in both of your names! Not only is it linked to both names, most likely you’re both contributing to this in one way or another.

It’s just plain rude to not chat with that person and what their thoughts are on the purchase. You need to respect your accounts as you would want your relationship to be respected. Don’t be that person who only looks out for themselves. You’re in this together.

Shall I get the steak, or the lobster?

Let’s face it…sometimes in life, there is a time to splurge and have fun with the money you have earned. When that time comes, choose wisely and enjoy spending the money in a responsible and fun way of your choice.

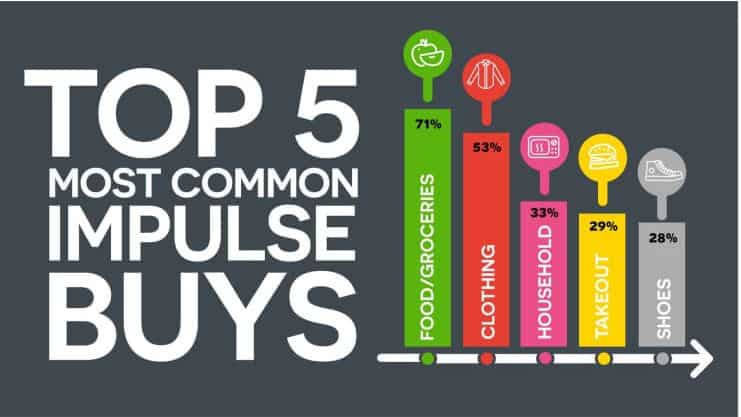

Impulse Spending Is Literally Eating Our Budgets!

Did you know it’s reported that impulse spending accounts for about $5400 a year for the average American? (source CNBC)

- The largest group of impulse purchases are made by younger American Adults averaging from ages 18 – 29.

- Of that group, more single persons make impulse buys.

- In most age groups, men are more likely to make an impulse purchase.

- Over 70% of impulse purchases are on groceries. (someone needs to learn meal planning)

Try my wait and see method?

Basically, you research then research (crowdsource your info!) , determine, then wait.

BEFORE you begin, be sure you’re signed up for all the cashback site, they also have competetive offers you can compare when you find your perfect price.

When I want something I stalk pricing online, ask around if my friends on social media think it’s the ‘best deal’? Seriously social media is the best for this. Ask in your own ‘friends’ or social circles so you know it’s from likely trusted sources.

Research the product reviews and if there are other products that can do the same in similar price ranges.

Ask around for what others have paid, what’s the best price they’ve seen. Determine your ‘Fair” price point.

Now back to some research. Google on ‘best time to buy’ for your product. Yup, even kitchen gadgets have a season that it’s best to purchase.

Now comes the waiting. Wait til your product comes on sale. This is seriously when the most savings come in. Half the time you realize this was an impulsive want and you no longer want or desire this item. How’s that for scoring 100% savings!

Not long ago, I decided I wanted to buy a camera. I waited almost 6 months to buy. Not just for the best price but also to be sure spending about $500 was really what I was prepared to do with my hard-earned money.

Too often I want something, but when I wait it out I determine I could get by with less and that money goes towards something more important like reducing debt or increasing savings.

Related: What Should an Emergency Fund Be Used for (And NOT Used for)

Conclusion

No matter what questions you need to ask yourself to better understand why you want, or need, to spend money, find what works for you. Pay attention to your spending trends to see if you can get a better understanding of your money habits. By asking a few of these harder questions, it can help in thinking and processing if spending money is truly a need, a want, or a habit.

“What’s the sense in buying something that doesn’t bring you joy or worse if it creates financial anxiety ? If it’s a purchase for convenience reasons, ask yourself how often will you use it and will you truly enjoy this product. Will it be worth your money? Is there a better reward to be had by saving ?

The good news is that if we are mindful of our spending habits, we can save some hard-earned cash while also feeling satisfied with what we have purchased! With these tips on hand next time you go shopping, nothing should stop us from enjoying life without being weighed down by debt or regretful purchases again!